.svg)

After two years of correction, the global fintech sector has not just recovered -- it has matured. Global fintech revenues hit $504 billion in 2025, growing more than four times faster than traditional financial services. But the more important story is not the size of the rebound. It is what is driving it: real profitability, selective investment, and a fundamental shift in how financial services are built and delivered.

This report from Boston Consulting Group and FT Partners is the clearest picture yet of where financial technology is headed -- and what it means for the people and institutions managing wealth today.

By the numbers

The shift in investor behaviour is equally telling. Late-stage funding (Series E and beyond) grew over 210% from 2023 to 2025, while seed-stage funding contracted by 10%. Capital is concentrating around companies with proven economics, not early-stage bets. The fintech spring, as the report puts it, is in full bloom -- but it rewards execution, not just ambition.

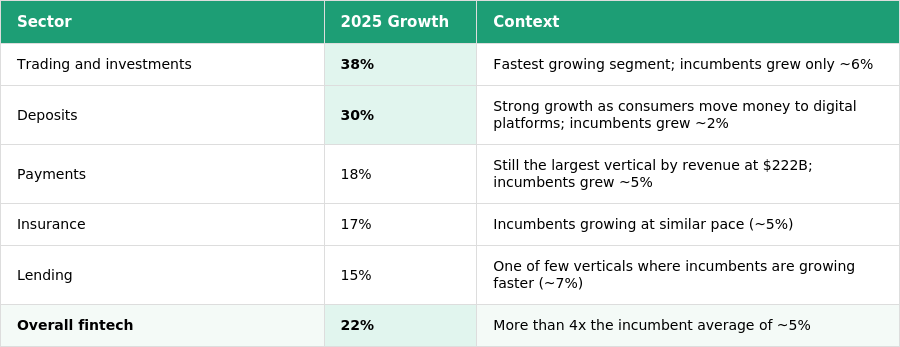

Where the growth is coming from

Not every part of fintech is growing equally. Trading and investments and deposits are the standout performers, while payments -- though still the largest vertical -- is maturing.

Asia-Pacific led regional growth at 25%, driven by digital banking and crypto platforms in Japan, South Korea, Singapore, and Indonesia. Europe grew 24%, supported by neobanks expanding into adjacent products. North America grew 21%, broadly in line with the global average. Latin America, while growing at 15% in 2025, has the highest compounded growth rate since 2021 at 44%.

The single biggest untapped opportunity in the entire report is B2B financial services. Fintechs have barely scratched the surface of business lending, insurance, and deposits. Workflows like accounts payable, expense management, and reconciliation are still largely manual. The platforms that crack this will define the next decade of fintech growth.

Profitability is real and improving

The profitability story is equally striking. Among the 85 largest public fintechs, average EBITDA margins reached 20% in 2025 -- up 4 percentage points in a single year. This is not a sector scraping by on growth promises. It is a sector earning its place.

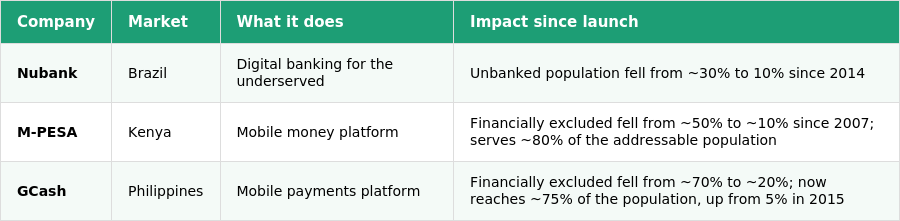

Fintech is closing the financial inclusion gap

One of the most compelling sections of the report is not about revenue or funding. It is about reach. Fintech has become one of the most powerful tools for expanding financial access in emerging markets -- and the numbers are remarkable.

These are not niche outcomes. They are proof that when the market structure and distribution model are right, fintech can move from niche disruption to mass-market utility -- and do so in under a decade.

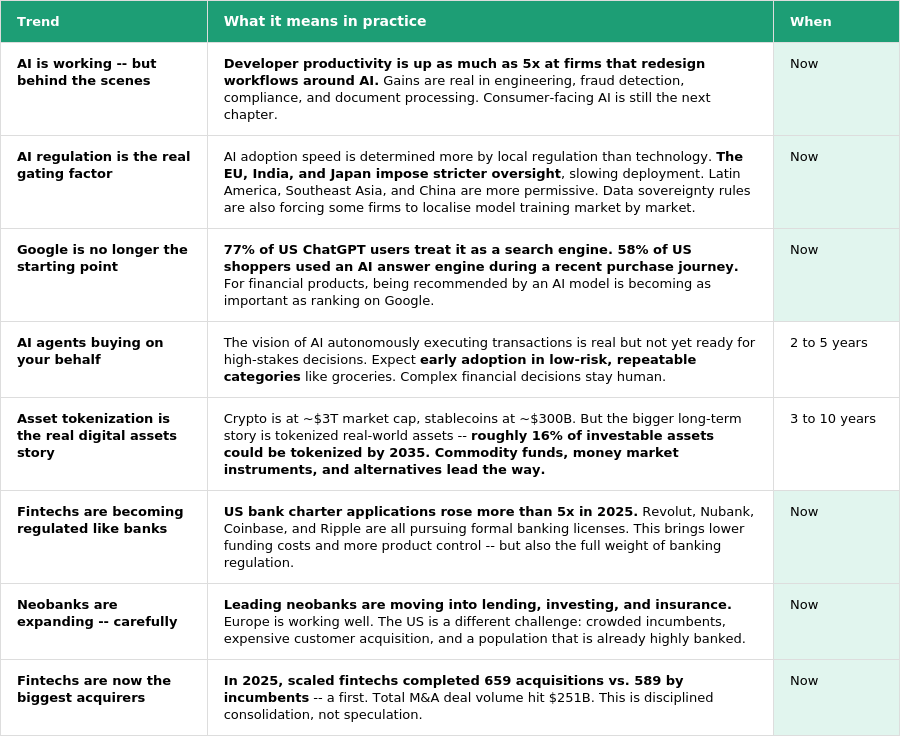

Seven trends every wealth manager should understand

The report identifies seven forces that will shape who wins and loses in financial services over the next five years. Here is what they mean in plain terms.

The exit market is opening -- selectively

Fintech IPOs rose 50% in 2025, from 28 to 42. M and A deal volume hit $251 billion, up from $184 billion the year prior. For the first time on record, scaled fintechs completed more acquisitions than incumbent banks.

But public markets remain demanding. The 30 largest fintech IPOs of the past five years have underperformed the broader financial services sector by roughly 24 percentage points in annual total shareholder returns. Investors are still pressing hard on profitability, customer concentration, and compliance maturity. The bar to go public has risen significantly.

What this means for family offices and wealth management

The report makes a compelling case that the tools once reserved for the largest institutions are now accessible to everyone. That shift has direct implications for how family offices and high-net-worth individuals manage wealth.

- Structured data is the foundation of everything. AI delivers value only when the underlying data is unified, clean, and organised. Platforms that have built structured data foundations are disproportionately positioned for AI-driven capabilities.

- Integration is no longer optional. The problem of maintaining parallel records across a wealth platform and an accounting system creates reconciliation risk and wasted time. Direct integration between systems is fast becoming table stakes.

- B2B and family office technology is the next frontier. The report is explicit that B2B financial services is the most underpenetrated segment in fintech. Family office technology -- historically fragmented and manual -- sits squarely in this white space.

- Regulatory maturity is a good thing. Clearer rules around AI, digital assets, and banking charters reduce uncertainty and create a more predictable environment for platforms building long-term infrastructure.

- Execution speed is the durable moat. As the report notes, AI tools will eventually be available to everyone. What separates winners is how quickly and effectively they deploy them across real workflows.

MyFO is purpose-built for this moment. By connecting entities, assets, cash flow forecasting, document management, accounting integration, and task workflows into a single structured data layer, MyFO gives family offices the foundation that makes AI genuinely useful -- not just a feature, but an operating advantage. The report's conclusion is clear: the platforms that unify data and automate workflows today will be the ones that compound that advantage for years to come.

-------------------------------------------------------------------------------------------------------------------------------------------------------------

All statistics are sourced directly from the BCG + FT Partners Global Fintech Report 2026, 4th Edition (June 2026). Data from S&P Capital IQ, Pitchbook, BCG FinTech Control Tower, and BCG Banking and Insurance Revenue Pools. This post is a summary interpretation of publicly available research and does not constitute financial advice.

.png)

.png)

.png)

.png)